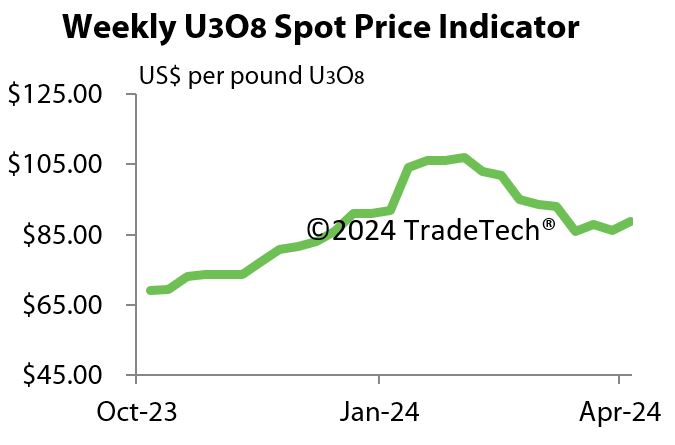

The following content is excerpted from the Management's Discussion & Analysis of Uranium Participation Corp. dated June 27, 2018 filed on SEDAR.

Uranium Industry Overview (March - May 2018)

During the quarter (March - May 2018), the uranium spot price has reacted to a series of recent developments suggesting

improving fundamentals for the uranium market. At the end of May 2018, the spot price for uranium reached a high of

US$22.75 per pound U3O8. Subsequent to the end of the quarter, uranium prices continued to rise, reaching a high of

US$23.40 per pound U3O8, before retreating to US$22.55 per pound U3O8 as of June 27, 2018.

The market narrative has turned more positive, in part, based on an acceleration of global production cuts. Based on

announcements from uranium producers, upwards of 30 million pounds U3O8 in annual uranium supply has been

removed from the market since 2016. A growing number of uranium producers have decided to reduce production in

light of low prices, which on the spot market remain below the production costs of the large majority of global uranium

mines. The expiration of older legacy contracts has contributed to this trend, as production protected by higher price

contracts is rolling off. UxC Consulting reports that worldwide production peaked in 2016 at 162 million pounds, fell to

154 million pounds in 2017, and is expected to drop below 135 million pounds in 2018. This is in comparison to projected

2018 uranium demand of 192 million pounds.

Paladin Energy Ltd. is the latest to producer to announce a reduction in supply, declaring that its Langer Heinrich Mine

in Namibia, with an annual production level of over 3 million pounds U3O8, will go on care and maintenance, in response

to prolonged low uranium price levels.

The United States Department of Energy has also contributed to reduced supply by putting a hold on their uranium

inventory barter sales, as a result of unrelenting pressure from the domestic uranium industry. This is expected to

remove over 3 million pounds of U3O8 in supply from the market on an annual basis.

Cameco Corp. recently announced that it had yet to embark on the spot market purchases that will be

required to meet its contracted delivery commitments, following the previously announced 10 month shutdown of its

MacArthur River Mine/Key Lake Mill complex. Cameco is also expected to make a decision later this year on whether

to extend the shutdown of MacArthur River/Key Lake, beyond the originally announced 10 month period ending October

2018.

Also contributing to the rebalancing of the uranium market has been the continued production constraint demonstrated

by National Atomic Company Kazatomprom and operations in Kazakhstan, which account for 40% of

global uranium supplies. Kazatomprom recently disclosed that its announced 10% production decrease for 2017 proved

to be closer to 5.5% given the late implementation of the cuts at various operating centers and joint ventures.

Kazatomprom has, however, restated its intention to cut 20% from 2018-2020 planned production levels, and is taking

a more consultative approach with its partners to better achieve this objective. In fact, recent Kazakh government and

industry announcements are indicating 2018 production targets that are expected to amount to a reduction of 3.4 million

pounds compared to 2017 actual production.