The following content is excerpted from the Management's Discussion & Analysis of Uranium Participation Corp. dated September 27, 2018 filed on SEDAR.

Uranium Industry Overview (June - August 2018)

The global nuclear power industry recently met at the World Nuclear Association's ('WNA') annual symposium in London, UK, where the atmosphere reflected a more positive mood towards the uranium market in general - supported in large part by continued production curtailments. Significantly, the announcement that Cameco Corporation's ('Cameco') McArthur River mine will be shut down indefinitely, removing up to 18 million pounds of U3O8 production from the market annually, has reaffirmed that primary uranium production will remain in a deficit to annual demand for the foreseeable future.

High levels of spot market purchasing, which have already exceeded 63 million pounds U3O8 for calendar 2018, have also contributed to the positive sentiment. Spot purchases have been made by a mix of utility buyers, traders, financial vehicles, including UPC, and primary producers. Cameco, for example, has publicly confirmed its intent to purchase 9 to 11 million pounds of uranium in the spot market before the end of calendar 2019. UxC reported in September 2018 that a producer issued a request for proposals ('RFP') to purchase 500,000 lbs U3O8.

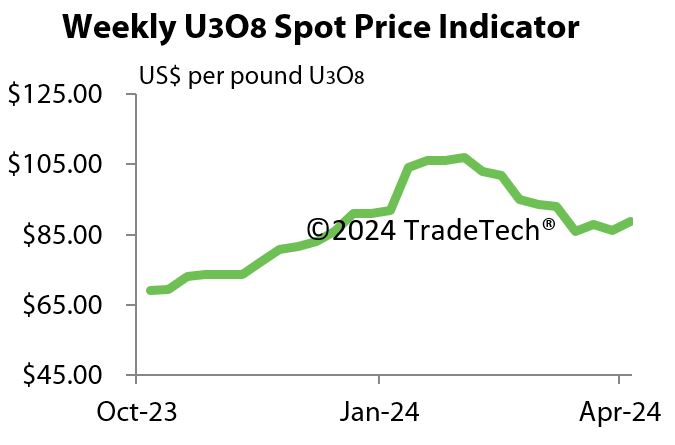

The positive market sentiment has been reflected in the uranium spot price, which ended the quarter at US$26.20 per pound U3O8, up from US$22.75 per pound at May 31, 2018. Subsequent to the end of the quarter, the spot price has continued to rise, breaking through the US$27 per pound U3O8 threshold at the beginning of September 2018.

On the demand side, the ongoing investigation into the Section 232 trade petition filed in the United States continues to create a sentiment of uncertainty with US and global utilities. This uncertainty is believed to be contributing to the lack of positive momentum in the long-term contract price for uranium, despite the steady increase in the spot price.

The conversion market has also continued to strengthen in the recent months, following the shutdown of Honeywell's ConverDyn conversion facility in Metropolis, Illinois, and the closure of Orano Group's ('Orano') Comurhex conversion plant in France. Orano is transitioning to its new Philippe Coste conversion facility, which officially opened in September 2018, and which is expected to slowly ramp up production, not reaching full capacity until 2021.

The uranium industry was also impacted by other international market events. In France, where nuclear power plants account for roughly 75% of the country's energy generating capacity, a new energy and environment minister has been appointed following the sudden departure of Nicolas Hulot. His replacement, Francois de Rugy, has generally been reported to be more even-handed regarding nuclear power policy than his predecessor - which is considered a positive development, as the French government is still reportedly seeking to reduce its nuclear capacity to 50% of electricity generation. The draft of a new energy plan is expected this fall, which could clarify these goals. In addition, in Kazakhstan, the market is still waiting to see when National Atomic Company Kazatomprom's highly anticipated IPO will proceed, and how it will affect the uranium industry both domestically and globally.